Australia’s economy, once a global symbol of stability and growth, is now showing signs of strain, facing its slowest pace of economic expansion in decades. What was once seen as the envy of the developed world, particularly during the 2007-2009 Global Financial Crisis when the country managed to avoid a recession, is now struggling to keep up with its international peers.

Racheal Clayton, a 22-year-old graduate from Sydney, finds herself caught in the changing economic landscape. While attending primary school during the height of the global financial crisis, Australia was emerging as an economic success story. Now, as she navigates the world of work, the optimism surrounding Australia’s economic future seems to be fading. Clayton, like many of her peers, is pessimistic about the country’s economic outlook. She works full-time in public relations but has had to pick up a part-time job as a personal trainer to cover her expenses. Despite living with her parents and not having to pay rent, Clayton still struggles with rising costs for food, bills, insurance, and maintaining a car.

In 2024, Australia’s economic growth has stagnated, growing at just 0.8 percent year-on-year during the first three quarters. In comparison, other major economies like the United States and the Eurozone posted growth rates of 3.1 and 0.9 percent, respectively. If not for immigration-driven population growth, the country would have slipped into a recession, as per capita growth has been negative for seven consecutive quarters. Australia’s slowdown follows a broader global trend, but the country’s struggles seem especially pronounced in key areas such as wage stagnation and property affordability.

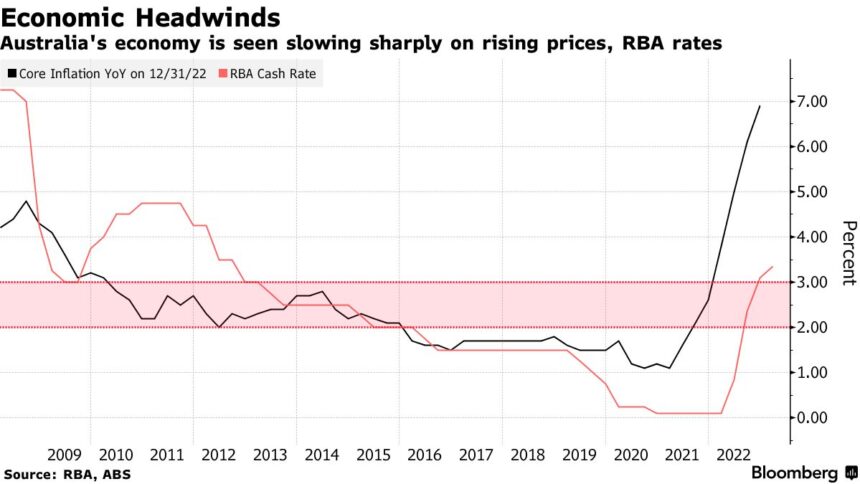

Australia’s inflation surged to a high of 7.8 percent in December 2022, while wages stagnated. Real wages, according to the Organisation for Economic Co-operation and Development (OECD), are still 4.8 percent lower than pre-pandemic levels. With property prices reaching record highs, many Australians like Clayton are finding it increasingly difficult to save for a home, a sentiment echoed by young people across the country. The cost of living is at a critical point, with many struggling to secure financial security, let alone the prospect of homeownership.

After coming out of a 1990s recession, Australia enjoyed a remarkable 28-year period of uninterrupted economic growth, until the COVID-19 pandemic hit in 2020. Since then, the economy has found it challenging to recover, with higher interest rates, falling productivity, and reduced demand for exports such as iron ore. The Reserve Bank of Australia (RBA) has increased interest rates in a bid to tame inflation, but these hikes have put pressure on mortgage holders, contributing to a reduction in consumer spending. A recent survey by the Salvation Army found that one in four Australians were concerned their children would miss out on Christmas presents, while 12 percent feared their children might go without food.

The effects of the interest rate hikes are evident in rising mortgage payments. After lowering rates to near zero during the pandemic, the RBA raised the rate to 4.35 percent in a series of steps aimed at addressing inflation. However, the rate hikes have had a chilling effect on consumer spending, which accounts for more than half of Australia’s GDP. Senior economist Matt Grudnoff from the Australia Institute warned that low consumer spending was a major factor in the sluggish economic growth.

Another contributing factor to the current economic difficulties is Australia’s housing supply shortage, which is pushing property prices and rents higher. The National Housing Finance and Investment Corporation (NHFIC) estimates that Australia will face a shortfall of 106,300 homes by 2027. This ongoing housing crisis, combined with a lack of affordable properties, is adding to the strain on many households.

In response to the rising cost of living and labor shortages, the Australian government has proposed reducing immigration levels to ease pressure on housing and infrastructure. The Labor Party government, which took office in 2022, announced plans in 2023 to cut the intake of permanent migrants to pre-pandemic levels and proposed capping international student arrivals. This decision is seen as an attempt to address the strain on resources caused by record-breaking migration levels. However, experts such as Trent Wiltshire, deputy director at the Grattan Institute, argue that migration is not the root cause of Australia’s economic problems. Instead, the country’s lack of productivity growth and failure to diversify its economy post-pandemic are major contributing factors.

Independent economist Nicki Hutley noted that successive governments have failed to make investments in growth drivers, such as green energy, and have instead spent on short-term measures, such as building houses that would have been constructed anyway. According to Hutley, Australia’s economy, while small and open, is heavily reliant on countries like China, and the country needs to diversify its markets and encourage investment in future growth areas to ensure long-term economic stability.

As Australia looks to the future, many experts agree that the country’s economic performance depends on implementing productivity-enhancing reforms and creating a more robust and diversified economy. While immigration has played a role in supporting growth, it is clear that Australia needs to address deeper structural issues if it is to regain its status as an economic powerhouse. With federal elections on the horizon in 2024, the decisions made in the coming years will be crucial in determining whether Australia can overcome its current economic challenges and restore its reputation on the global stage.