Despite strong corporate profits and healthier bank balance sheets, India’s private investment remains sluggish. This seeming paradox—where companies are making money and banks are ready to lend, yet capital formation is muted—points to deeper structural issues in India’s economy. A closer look reveals that large firms are not necessarily holding back; they are investing at levels that reflect their moderate expectations for future growth. To change this, India needs a new wave of economic reforms—especially in land markets—to unlock its next phase of growth and global competitiveness.

The Growth-Investment Disconnect

India’s real GDP growth for FY2025–26 is projected between 6.3% and 6.8%, notably lower than the previous year’s 8.2%. It’s still uncertain whether this dip marks a temporary pause or a long-term slowdown. One way to assess the economy’s structural strength is by looking at gross capital formation, which has hovered around 30–32% of GDP in recent years. To reach the aspirational 8%+ annual growth target required for Viksit Bharat@2047, this investment rate must rise to 35% or more.

Yet, the private corporate sector, which typically drives the capital expenditure (CapEx) cycle, has not returned to its investment peak. Between 2004 and 2008, during India’s high-growth years, corporate investments averaged 16% of GDP. In FY2022–23, this figure was just 12%.

Why Is India Inc. Holding Back?

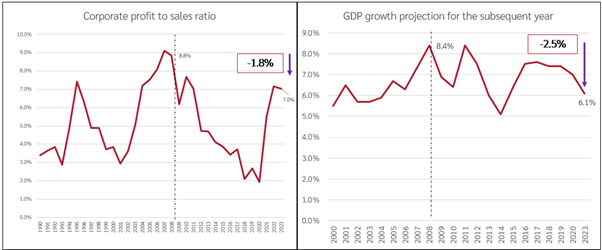

At first glance, it’s puzzling: corporate profitability is back to peak levels. The net profit-to-sales ratio is 7% in 2023—double the average of the past decade and similar to the golden years of 2004–2008. Banks too are healthy, with non-performing assets down to 2.6%. In theory, the conditions for investment are strong.

But while profitability reflects companies’ ability to invest, actual investment depends on their willingness, which is driven by their expectations of future demand. Today, with a modest growth outlook of 6.5%, firms are cautious. In contrast, back in 2004–2008, when growth expectations were closer to 8%, corporate confidence was much stronger. In short, companies are not irrationally withholding investment—they’re making rational decisions based on tepid demand projections.

Exports and Growth Expectations

A big factor behind these muted expectations is weak export growth. Between 1994 and 2008, India’s real exports surged, and so did GDP growth. But between 2012 and 2020, export growth slumped to just 3.5%, dragging down GDP growth with it. While exports have seen some recovery, the outlook for global trade remains subdued due to geopolitical fragmentation and rising protectionism.

For India to grow faster in this sluggish trade environment, it must boost export competitiveness—which requires systemic reform.

The Role of Large Firms

Large firms are central to driving exports. Around 55% of India’s exports come from large companies—higher than the 40–45% share in many developed economies. But over 85% of Indian large firms’ revenues come from the domestic market. In countries like South Korea or France, this figure is around 70–75%. The limited international presence of Indian firms is not due to lack of ambition but due to domestic structural bottlenecks that make them less competitive globally.

What’s Holding Indian Firms Back?

India’s regulatory environment raises the cost of doing business. Key issues include:

– Restrictive labour laws that require prior approval to retrench workers in firms with over 100 employees.

– Higher real interest rates compared to countries like China.

– Expensive and inaccessible land, especially in urban areas.

These challenges make Indian firms less agile and more costly. As a result, they often split operations across multiple smaller plants and shift away from urban centers to avoid high land costs—creating a fragmented industrial landscape that lacks the productivity advantages of urban agglomerations.

In contrast, countries like China have benefitted enormously from concentrated growth models. Major cities like Shanghai and Beijing have per capita GDPs significantly higher than Indian cities like Mumbai or Delhi, despite comparable population sizes.

The Missing Reform: Land

Among all the factors of production—land, labour, capital, and entrepreneurship—land remains the most under-reformed. Unlocking land supply and improving affordability is essential. Reforms should focus on:

– Transparent land use and digitised ownership records.

– Expanding the supply of developable land.

– Enabling real competition in real estate to bring down prices.

– Using public land (owned by the government) to set an example in reform.

Affordable land enables not just industrial expansion but also better housing and urban planning—critical for dignified living, labour mobility, and job creation. A transparent and efficient land market can reduce housing cost burdens, lower the price-to-income ratio, and improve urban productivity.

A New Growth Model for a New Era

India has the opportunity to build a globally competitive industrial base by reforming land and making its firms more export-ready. With limited room for global trade expansion, the only way India can carve out a larger share is by being more competitive than others. Large Indian firms must be empowered to build scale, productivity, and international reach.

By improving land access and affordability, the country can reduce input costs, improve urban industrial ecosystems, and boost both exports and investment. Reforms in labour and capital are important—but land cannot be left behind.

India’s next big investment revival depends not just on macroeconomic stability or bank lending, but on a bold new chapter of reforms—starting with land.